Weekly Market Updates

“Computer Tutor”

“There must be ONE stock somewhere that’s a buy,” we said. You see, even computer people are victims of these old atavistic instincts from the pre-computer days. The computer just folded its arms. It wouldn’t buy anything. Then, just when we were worried that it would never buy anything, right at the bottom it stepped in and started buying. The market started going up, and the computer kept on buying. Pretty soon the computer was fully invested and the market was still going up.

“What did it do then?” I asked. “The market was still going up,” Irwin said, “and then one day it came AND ASKED US FOR MARGIN. It wanted to keep buying. So we gave it margin. After the market went up some more it sold out of a bit, but came back to being fully invested; right now it has still got buying power.” “Irwin,” I said, “tell the truth now. If all these computers go on air, as you say, does an individual investor have a chance?” “There’s always luck,” Irwin said. “Luck — which is to say a serial run of random numbers – can happen any time. And the computer is out for really aggressive performance. An individual, with a longer time horizon, might be able to do passably.”

— Adam Smith, “The Money Game” (1968)

We have used the aforementioned quip from our departed friend Jerry Goodman (aka Adam Smith) a number of times over the past 47 years because of the wisdom it imparts. We dredged it up this morning after reading an article in Barron’s over the weekend titled, “Man and Machine,” which was an interview with Omar Selim, the CEO of Arabesque Asset Management, a quantitative and sustainable investment management firm. In a quantitative investment fund, customized computer models are built using software programs to determine the fund’s investments. Over the past number of years there has been an increasing move by firms to build investment management software and to turn over the management of money to the “machines.” We remember the first quantitative investor, namely Dean Lebaron, who founded Batterymarch in 1969. Dean hired computer “rocket scientists” from NASA to build the models that guided the investments of Batterymarch, and it worked. However, Dean made some VERY key macro decisions on what said computers were supposed to look for in an investment. For example, in the early 1980s Dean “told” his computers to stop looking for investments in “hard assets” and switch to looking for companies that play to financial investments. That was a pretty key macro shift as short-term interest rates were set to collapse, causing financial assets to soar. So it begs the questions, “Do machines, in and of themselves, really have intelligence?” We think the answer is no, although they are certainly a great tool in aiding in the investment process.

As written by us a number of years ago:

Ladies and gentlemen, the computer has no possibility of foreseeing things that may occur, especially out-of-the- blue events (black swans) that catch humans by surprise. Certainly you can feed a computer historical data and set up a series of “what ifs” for potential happenings based on past experiences. But how do such past data- points help us foresee the Ukraine Upset? How do you program for rumors that move markets? How does the recent massive M&A trend affect select companies’ valuations? The computer cannot predict the when, the where, the how of such events, or what the consequences are that follow. If the human mind cannot foresee things that defy conceptual imagination, how can they program that into a computer?

To be sure, we too have computer-based models, but many times we override those models when our 54 years of investment acumen, and 47 years in this business, suggest going counter to the models. This is especially true when the short-term, and intermediate-term, models are conflicted, which has been the case for months up until Thanksgiving week. Ever since then we have embraced the mantra, “It is tough to put stocks away to the downside in the ebullient month of December,” and that was the case again last week.

For the week the D-J Industrials, and S&P 500, both closed up by roughly 0.40%; but, the big winner for the week was the D-J Transports, which was better by more than 2%. The Trannies’ outperformance was likely attributable to the stronger economic reports and a 1.78% decline in crude oil prices. In fact, in a statistical oddity, ALL of the commodities we monitor closed down for the week. Despite that Weekly Wilt, we think most of the commodities we study are on “buy signals.” Thus, we are not surprised that the U.S. Dollar Index is on a sell signal. The biggest winning sector on the week was Financials (+1.5%), while Utilities (-1.03%) was the biggest loser.

The call for this week: Since 1928 the S&P 500 Index has been up 65 times in the month of December, with an average gain of 3.0%, and down 24 times. We think that strength will continue into the new year. Indeed, as our friend and portfolio manager Michael Mulling of the Atlanta-based Stonewall Asset Management titled a recent letter to clients, “December is no month to be out of the market.” He goes on to write:

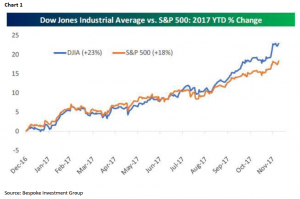

- Isn’t it better to wait for stocks to correct, then buy them? Yes of course it is! However in doing so you have to make TWO critical decisions. When to sell them and go to cash and then when to get back into stocks. That would not have worked this year as the most the broad market has declined is around 3%. The opportunity lost could be substantial. See the November 2017 chart above to WHAT MAY HAVE BEEN MISSED (see chart 1 on the next page).

- Is there a prudent way to take some money off the table in stocks and go to cash? Yes of course there is! If you and your Financial Adviser set a goal of 60% in Stocks/Funds and the appreciation of your stock portfolio has grown to 70%, trim or sell 10% from stocks and go to cash or bonds. You can have that portion stay in cash or if the market declines 10%, redeploy that back into stocks. Sell High, Buy Low? Now that’s the ticket!

- How can I decide when to redeploy my stock sales that are in cash accounts like money market or short term treasury bonds back into stocks? GOOD QUESTION! Instead of waiting for a market correction that may not come for a while and then when a correction does happen, many are worried it will go lower and any decision to reinvest into stocks at that time is frozen, try this. Set a percentage of your cash each month or quarter to go back into stocks or funds. On individual stocks, place limit orders. On mutual funds, do not worry about the timing. Owning many stocks in many industries is a good long term strategy. It has been a sound and prudent wealth accumulation plan for many decades.

P.S.: As Andrew and I have said for nine years, “It’s a bull market you know, with years left to run!”

Important Investor Disclosures

Raymond James & Associates (RJA) is a FINRA member firm and is responsible for the preparation and distribution of research created in the United States. Raymond James & Associates is located at The Raymond James Financial Center, 880 Carillon Parkway, St. Petersburg, FL 33716, (727) 567-1000. Non-U.S. affiliates, which are not FINRA member firms, include the following entities that are responsible for the creation and distribution of research in their respective areas: in Canada, Raymond James Ltd. (RJL), Suite 2100, 925 West Georgia Street, Vancouver, BC V6C 3L2, (604) 659-8200; in Europe, Raymond James Euro Equities SAS (also trading as Raymond James International), 40, rue La Boetie, 75008, Paris, France, +33 1 45 64 0500, and Raymond James Financial International Ltd., Broadwalk House, 5 Appold Street, London, England EC2A 2AG, +44 203 798 5600.

This document is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The securities discussed in this document may not be eligible for sale in some jurisdictions. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Investors should consider this report as only a single factor in making their investment decision.

For clients in the United States: Any foreign securities discussed in this report are generally not eligible for sale in the U.S. unless they are listed on a U.S. exchange. This report is being provided to you for informational purposes only and does not represent a solicitation for the purchase or sale of a security in any state where such a solicitation would be illegal. Investing in securities of issuers organized outside of the U.S., including ADRs, may entail certain risks. The securities of non-U.S. issuers may not be registered with, nor be subject to the reporting requirements of, the U.S. Securities and Exchange Commission. There may be limited information available on such securities. Investors who have received this report may be prohibited in certain states or other jurisdictions from purchasing the securities mentioned in this report.

Please ask your Financial Advisor for additional details and to determine if a particular security is eligible for purchase in your state.

The information provided is as of the date above and subject to change, and it should not be deemed a recommendation to buy or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. Persons within the Raymond James family of companies may have information that is not available to the contributors of the information contained in this publication. Raymond James, including affiliates and employees, may execute transactions in the securities listed in this publication that may not be consistent with the ratings appearing in this publication.

Raymond James (“RJ”) research reports are disseminated and available to RJ’s retail and institutional clients simultaneously via electronic publication to RJ’s internal proprietary websites (RJ Investor Access & RJ Capital Markets). Not all research reports are directly distributed to clients or third-party aggregators. Certain research reports may only be disseminated on RJ’s internal proprietary websites; however such research reports will not contain estimates or changes to earnings forecasts, target price, valuation, or investment or suitability rating. Individual Research Analysts may also opt to circulate published research to one or more clients electronically. This electronic communication distribution is discretionary and is done only after the research has been publically disseminated via RJ’s internal proprietary websites. The level and types of communications provided by Research Analysts to clients may vary depending on various factors including, but not limited to, the client’s individual preference as to the frequency and manner of receiving communications from Research Analysts. For research reports, models, or other data available on a particular security, please contact your RJ Sales Representative or visit RJ Investor Access or RJ Capital Markets.

Links to third-party websites are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any third-party website or the collection or use of information regarding any website’s users and/or members.

Additional information is available on request.