Weekly Market Updates

Investment Strategy: “Losses!?”

Everyone knows how to win. Few know how to lose. Yet the secret to making money in the various markets is knowing how to lose. How to control your losses. In the book Warren Buffet calls the best book ever written on investing, namely Ben Graham’s The Intelligent Investor, it notes, “The essence of portfolio management is the management of risks, not the management of returns. All good portfolio management begins and ends with this premise.” My father put it much more succinctly when he said, “Son, if you manage the downside in a portfolio, and avoid the big loss, the upside takes care of itself.” Indeed, knowing how to lose, how to control your losses is the key to successful investing. Listen to the pros:

I’m always thinking about losing money as opposed to making money. Don’t focus on making money, focus on protecting what you have.

– Paul Tudor Jones

The majority of unskilled investors stubbornly hold on to their losses when the losses are small and reasonable. They could get out cheaply, but being emotionally involved and human, they keep waiting and hoping until their loss gets much bigger and that costs them dearly.

– William O’Neil

One investor’s two rules of investing:

- Never lose money

- Never forget rule number

– Warren Buffett

All of these professional investors have different market philosophies. They have contradictory strategies for making money. Some are traders; some are value players; some are growth-stock advocates, other are emerging-growth seekers, etc. But all of their messages are clear – learning how not to lose money is more important than learning how to make money! And, in learning how not to lose money you have to evaluate risk. Indeed, “The essence of portfolio management is the management of risks, not the management of returns!”

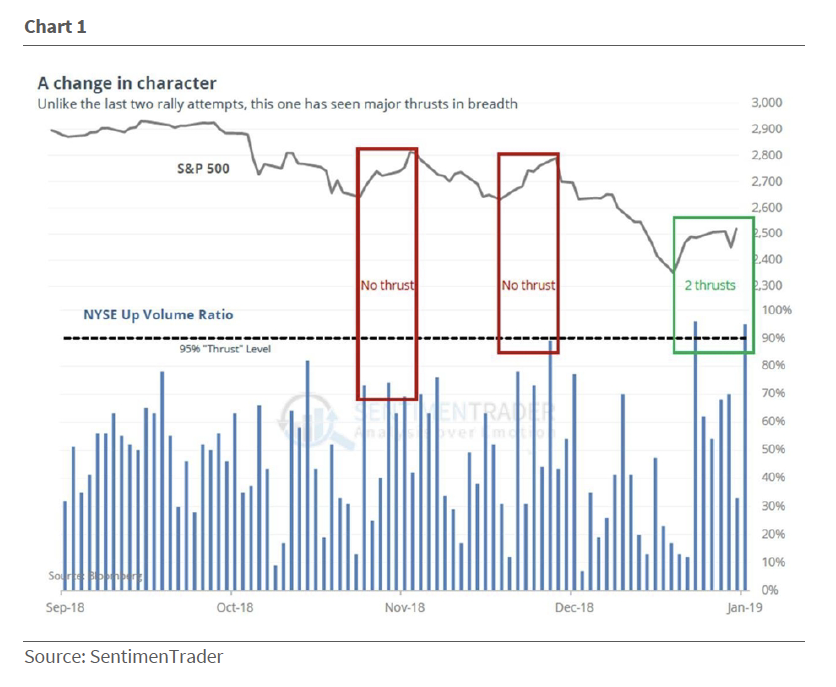

We revisit this “losses” topic because of what has happened over the past few months. The ~20% decline by the S&P 500 (SPX/2531.94) from our October 2 “sell signal” into the late December lows, which was much lower than we thought the decline would be, surprised us. While we said in early October to sell trading positions, we did nothing with investment positions that in retrospect we wish we had. That said, in late December the equity markets experienced the most oversold condition we have seen in a long time and we wrote about it. Of interest is that since late December we have experienced two 90% Upside Days whereby 90% of the total Upside to Downside volume has come on the upside. As the insightful Jason Goepfert (SentimenTrader) writes:

Unlike the nascent rallies in November and December, this time there has been a remarkable level of “oomph” behind the rallies. Within the past 10 days, there have been two sessions when more than 95% of all volume on the NYSE flowed into advancing securities. That’s among the best thrusts we’ve seen in 60 years. The only other times we’ve seen this were in August 1982, January 1987, and a few times during August – November 2011. All saw significant rallies over the next six months [see Chart 1].

Jason goes to write:

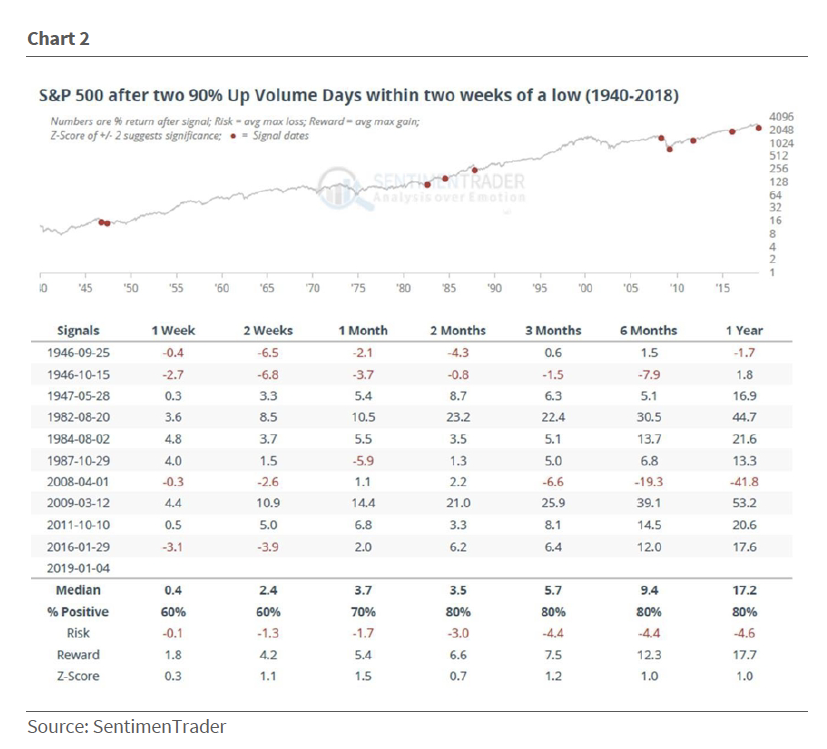

Adding to the impressiveness of the surge, this one also had the most Up Issues of any of the others in the past 60 years, other than for March 2009. Because the sample size is relatively small, if we eliminate the need for the S&P to have recently made a 52-week low before the thrust, then we get the signals in the following table. This was quite a bit more common and tended to be just as bullish for forward returns. Over the next six months, the S&P rallied 90% of the time, averaging 12%, nearly four standard deviations above a random six- month return since ’62 (chart 2). The only failure was in 2007-08. Based on how stocks have typically reacted to intense buying interest like this, we’d rate it as a medium-to long-term positive.

To us these “thrusts” suggest the intense selling seen in mid-December, combined with the breadth washout, imply we have made a significant low. Last Friday’s strength should set the stage for the SPX to challenge its overhead resistance level between 2600 and 2650 this week barring any unexpected news,

Speaking of politics, our friend Rich Bernstein (Richard Bernstein Advisors) concludes his recent letter with this:

One must remember that politicians are still politicians, and politicians typically have only one goal: get re-elected. Keeping that in mind, investors should keep their wits and realize there may be plenty of investment opportunities resulting from today’s uniquely unpredictable environment. In January, we’ll investigate those investment opportunities for 2019.

The call for this week: We received this from a portfolio manager over the weekend:

When you look at investor sentiment and positioning action we saw heading into the final weeks of the year it felt capitulatory given bearish sentiment we haven’t seen since the 2015-2016 growth scare yet over the past couple of weeks we have also seen a net contraction in 52 week lows on these mini retests since the oversold rally started 12/26. I think this is the market’s way of sending us an important message that the bottoming sequence has begun.

Stocks soared on Friday due to: 1) China’s verbal and actual intervention; 2) a surprisingly strong U.S. December NFP report (312K vs. 184K exp.); and 3) Fed Chair Powell exceeded even the most dovish expectations. This morning as we write the preopening S&P 500 futures are off 7 points on no real overnight news.