Weekly Market Updates

Investment Strategy: “What I Did on My Summer Vacation”

The place is appropriately named because it is not really a hotel, but rather a home with elegant furnishings, an art gallery populated with African art, a fabulous restaurant and wine bar, and a spa. Quite frankly, it is the home you wish you lived in. From there we drove to the wine country in Stellenbosch and Franschhoek, which actually felt like being in Switzerland. After a few days of wine tours we headed to Jeffreys Bay, one of the best surfing towns in the world, followed by a quick plane ride to Durban and Umhlanga where we stayed another must see hotel named The Oyster Box (Oyster Box). The highlight of the trip, however, was a safari at Zulu Nyala and Phinda (Zulu). To be sure, we saw most of the animals of South Africa and four of the “big five” because regrettably we never saw an African leopard (Big Five). For anyone wanting to go to Africa our advice is . . .GO.

So what’s happened in the various markets in our absence? Well, the answer to that question, from just looking at the averages, is not much. When we left the S&P 500 (SPX/2476.55) was changing hands around 2475 and as of Friday’s closing bell was trading at 2476. Beneath the surface, however, there have been a lot of moving parts. We had the Hurricane Harvey tragedy, more geopolitical situations: North Korea, Chinese “mischief” in the South China Sea, Nigeria, tensions between India and Pakistan, riffs between India and China, Brexit squabbles, potential tariffs on Chinese steel, NAFTA renegotiations, and of course the First Lady’s shoes (as the liberal “Daily Show” host Trevor Noah aptly said, “Here’s the thing, I don’t know why anyone should care what anyone wears when they’re on their way to help people.”).

Speaking to the hurricane horrors, we had one portfolio manager (PM) recite the famous French economist Frederic Bastiat’s (1801 – 1850) quip about the “broken window fallacy.” Said quip goes like this according to Investopedia:

In Bastiat’s tale, a man’s son breaks a pane of glass, meaning the man will have to pay to replace it. The onlookers consider the situation and decide that the boy has actually done the community a service because his father will have to pay the glazier (window repair man) to replace the broken pane. The glazier will then presumably spend the extra money on something else, jump-starting the local economy.

Bastiat goes on to explain why that is not true in the real economy. Likewise, the sagacious Caroline Baum stated in an article on MarketWatch (8-29-17), “No, hurricanes are not good for the economy – Yes, GDP may get a temporary boost from rebuilding, but there is nothing positive about destruction” (read the article here: Baum). That same PM suggested that thousands of trucks are now underwater, and since Texans love their trucks they will replace them, which should be positive for the truck manufactures. One positive thing coming out of this catastrophe is that it is now almost certain the debt ceil gets raised due to the billions of dollars in hurricane aid money that has been attached to the debt ceiling bill.

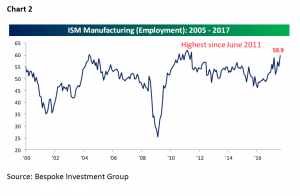

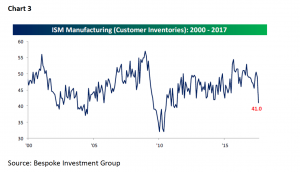

Also on the positive side Chinese export orders tagged their best levels in seven years, British manufacturing hit a four month high, the French manufacturing PMI orders rose at the fastest rate in years, and Greece and Italy are doing better as the world’s synchronized economic recovery continues. Here in our country the recovery is quite noticeable with the ISM Manufacturing Index reaching its highest level since 2011 (Chart 1). The ISM Manufacturing Employment Index confirms that strength with its highest reading since 2011 (Chart 2). Meanwhile, ISM Manufacturing (customers’ inventories) is plumbing lows, also not seen since 2011, implying future demand and further economic strength (Chart 3).

Also in “recovery mode” are earnings as the transition from an interest rate, to an earnings driven secular bull market, continues. As of last week, the S&P had the bottom-up operating earnings estimates for 2017 at $126.95 and at $144.67 for 2018 (as a sidebar, remember that every one point decline in the corporate tax rate hypothetically adds $1.31 to S&P 500 earnings). While those current S&P earnings estimates leave the SPX trading at 19.5x this year’s estimate, and 17.11x next year’s, in past missives we have presented arguments why price-to-earnings multiples (P/Es) should be higher than historic norms. We have also shown that P/E multiples are a pretty poor market-timing tool.

So, when we left for holiday in early August we opined that unlike the short-term trading advice we have used since two of our models flipped positive in mid-April – “to buy the dips” – was not operative this time. Once again, like in late-January, our short/intermediate models were “looking” for a 5 – 10% pullback. And, once again we have not gotten that, at least as of yet. What we did get was the same 2.8% pullback that we saw in the February to March pullback. What did happen in the recent drawdown was a break below the SPX’s “uptrend line” that has been in place since November of last year (Chart 4); and it also took that index below various moving averages. But again, just like in February and March, the SPX gathered itself together and re-rallied. Studying Chart 4 one ponders the question, “Is the SPX in the process of making a double-top in the charts, or is this the beginning of a new leg to the upside?” To answer that question we turn to our models.

To reiterate, our long-term model turned positive in October of 2008 and has never registered a bearish reading since. However, our short and intermediate-term models flipped negative in late-July/early-August, which prompted our trading call of, “We would not buy this envisioned dip.” So far that has proved wrong-footed. Compounding the current state of confusion is the fact that our short-term model went positive two weeks ago, but the intermediate-term model remains negatively configured. In the past, when this has happened, we have found it best to exercise the rarest trait on Wall Street – patience! Andrew Adams has repeatedly written about “patience” in our absence and we agree with him. In the not too distant future the equity markets will “tell” us what the correct strategy will be on a trading basis. Longer-term, we repeat “Old Turkey’s” advice from the book “Reminiscences of a Stock Operator,” “After all, this is a bull market!”

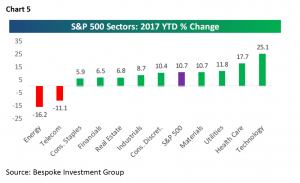

Moving on to the sectors, we have favored select macro sectors since our models called for a rally the week before the presidential election. Those favored sectors have been: Technology, Healthcare, Materials, Consumer Discretionary, Industrials, and Financials. Three of those sectors have outperformed the S&P 500, while three of them have not (Chart 5). Recently we have become very interested in Energy given the “selling exhaustion” readings on many energy stocks. With most of the energy complex trading at/new yearly lows, we think as tax loss selling season arrives portfolios should accumulate favored energy names. Finally, recently we have been hearing that tech is a very expensive sector after it huge rally, but this is just not true (Chart 6).

The call for this week: Gideon John Tucker wrote “No man’s life, liberty or property is safe while the Legislature is in session.” Those sage words are just as pertinent today as they were when first scribed in 1866. And, those words should be considered this week as Congress returns to D.C. with an uncertain legislative agenda. Adding to the uncertainty is North Korea’s successful hydrogen bomb explosion over the weekend. Our sense is that if there is going to be a downside feint it should begin this week. Certainly the seasonality is right for that with the D-J Industrials losing ~1.09% in the month of September 41% of the time. Also of note is that the August – November timeframe for years ending with the number “7” have a tendency to be a difficult time for stocks (1977, 1987, 1997, 2007 . . . 2017?). Moreover, the Momentum Indictor is short- term bearish, the Breadth Indicator is neutral, and the Sentiment Indicator is showing extreme complacency. This morning the preopening S&P 500 futures are down only 5.50 points despite renewed tensions on North Korea’s H-bomb success.

Typically the day after Labor Day is an “up” session, so traders will likely play for a rally emboldened by the UTX takeover of COL. We continue to exercise patience.

Important Investor Disclosures

Raymond James & Associates (RJA) is a FINRA member firm and is responsible for the preparation and distribution of research created in the United States. Raymond James & Associates is located at The Raymond James Financial Center, 880 Carillon Parkway, St. Petersburg, FL 33716, (727) 567-1000. Non-U.S. affiliates, which are not FINRA member firms, include the following entities that are responsible for the creation and distribution of research in their respective areas: in Canada, Raymond James Ltd. (RJL), Suite 2100, 925 West Georgia Street, Vancouver, BC V6C 3L2, (604) 659-8200; in Europe, Raymond James Euro Equities SAS (also trading as Raymond James International), 40, rue La Boetie, 75008, Paris, France, +33 1 45 64 0500, and Raymond James Financial International Ltd., Broadwalk

House, 5 Appold Street, London, England EC2A 2AG, +44 203 798 5600.

This document is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The securities discussed in this document may not be eligible for sale in some jurisdictions. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Investors should consider this report as only a single factor in making their investment decision.

For clients in the United States: Any foreign securities discussed in this report are generally not eligible for sale in the U.S. unless they are listed on a U.S. exchange. This report is being provided to you for informational purposes only and does not represent a solicitation for the purchase or sale of a security in any state where such a solicitation would be illegal. Investing in securities of issuers organized outside of the U.S., including ADRs, may entail certain risks. The securities of non-U.S. issuers may not be registered with, nor be subject to the reporting requirements of, the U.S. Securities and Exchange Commission. There may be limited information available on such securities. Investors who have received this report may be prohibited in certain states or other jurisdictions from purchasing the securities mentioned in this report.

Please ask your Financial Advisor for additional details and to determine if a particular security is eligible for purchase in your state.

The information provided is as of the date above and subject to change, and it should not be deemed a recommendation to buy or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. Persons within the Raymond James family of companies may have information that is not available to the contributors of the information contained in this publication. Raymond James, including affiliates and employees, may execute transactions in the securities listed in this publication that may not be consistent with the ratings appearing in this publication.

Raymond James (“RJ”) research reports are disseminated and available to RJ’s retail and institutional clients simultaneously via electronic publication to RJ’s internal proprietary websites (RJ Investor Access & RJ Capital Markets). Not all research reports are directly distributed to clients or third-party aggregators. Certain research reports may only be disseminated on RJ’s internal proprietary websites; however such research reports will not contain estimates or changes to earnings forecasts, target price, valuation, or investment or suitability rating. Individual Research Analysts may also opt to circulate published research to one or more clients electronically. This electronic communication distribution is discretionary and is done only after the research has been publically disseminated via RJ’s internal proprietary websites. The level and types of communications provided by Research Analysts to clients may vary depending on various factors including, but not limited to, the client’s individual preference as to the frequency and manner of receiving communications from Research Analysts. For research reports, models, or other data available on a particular security, please contact your RJ Sales Representative or visit RJ Investor Access or RJ Capital Markets.

Additional information is available on request.