Weekly Market Updates

“James Howard Kunstler?!”

It was back in November 2010 when James Howard Kunstler first wrote the aforementioned quote. We recalled that quote while spending last week in Nashville seeing institutional accounts and speaking at events for our financial advisors and their clients where the question du jour was, “What’s going on with the potential trade war?” In fact, one particularly clever client said, “Who cares about the price of tea in China!” Well, with what’s going on, everyone should care about what’s going on with China and the escalating rhetoric between the U.S. and China.

Speaking to the current spat, our friends at the brainy GaveKal organization penned a terrific white paper last week explaining things, which was titled “The Trouble With Trade Retaliation,” and written by Tom Holland:

So if China can’t impose countervailing tariffs, won’t devalue, and can’t dump its holdings of US debt, Beijing will have to look for another means of retaliation. The most obvious would be to target the businesses of large US companies operating in China.

So why can’t China impose “countervailing tariffs?” Well, it’s actually quite simple. If President Trump slaps another $200 billion in tariffs on China, with the threat of another $200 billion, that would bring the total to some $250 billion, consequently the math just doesn’t compute. Consider this, last year the U.S. imported roughly $500 billion of goods from China, yet China only bought $130 billion worth of U.S. goods. Given this mismatch, China can’t really retaliate in kind because it just doesn’t buy enough goods from the U.S.

As we surmised last week in one of our missives, “We doubt that China will devalue its currency.” Indeed, if China did so, it would cause massive outflows of capital from China’s financial system and likely impinge the renminbi’s credibility of one day becoming the world’s reserve currency, something Beijing has aspired to for a very long time.

Selling U.S. debt also should not work given the numbers. It is believed that China has ~$1.2 trillion of U.S. debt instruments. If China were to sell all of that at one time, it would surely raise rates in this country, but such a move is easier said than done. However, if they did, the buyer of last resort would be the Federal Reserve, who could obviously soak up the selling.

Moreover, as the good folks at GaveKal point out:

In the event, however, it is likely that Trump would invoke the 1977 International Emergency Economic Powers Act, which gives the US president all the legal authority he would need to freeze Chinese-owned treasury securities held by US custodians.

As for “targeting the businesses of large U.S. companies operating in China,” that appears to be the course China would attempt to take if provoked. Verily, in last week’s Global Times there was the mention of countermeasures against U.S. large cap companies that populate the D-J Industrial Average. Worth mentioning is that China has done this before by boycotting Japanese goods in 2012. Hereto, however, such actions could create even more problems for China. Again, as the good folks at GaveKal conclude:

In short, China has few attractive options. Retaliatory measures against US companies might damage their targets, but they will also destroy jobs, degrade competition and reduce productivity at home. That won’t stop Beijing pursing retaliation—it has done so before against Japanese and Korean companies. But the effectiveness of such retaliation will be limited, and the costs high.

As we wrote in last Friday’s Morning Tack, “Our D.C. contacts remain convinced China and the U.S. will work the Trade Tiff out over the coming months.”

Moving on to the stock market, heading into last week all of the major indices we monitor were over bought in the short run. Then on Tuesday the announcement of the potential for an additional $200 billion of tariffs on Chinese goods, with the threat of another $200 billion if China retaliates, lit the match with an attendant ~287 point Dow Dive. We did not expect the tariff announcement, nor did we expect Tuesday’s Tumble. Obviously our models were also caught by surprise. Subsequently we wrote, “Just like a heart attack patient doesn’t get right up off of the gurney and run the 100 yard dash, the stock market is likely going to have to convalesce for a few sessions without much further downside.” And, that is pretty much what happened as stocks limped into Friday’s closing bell. So what now?

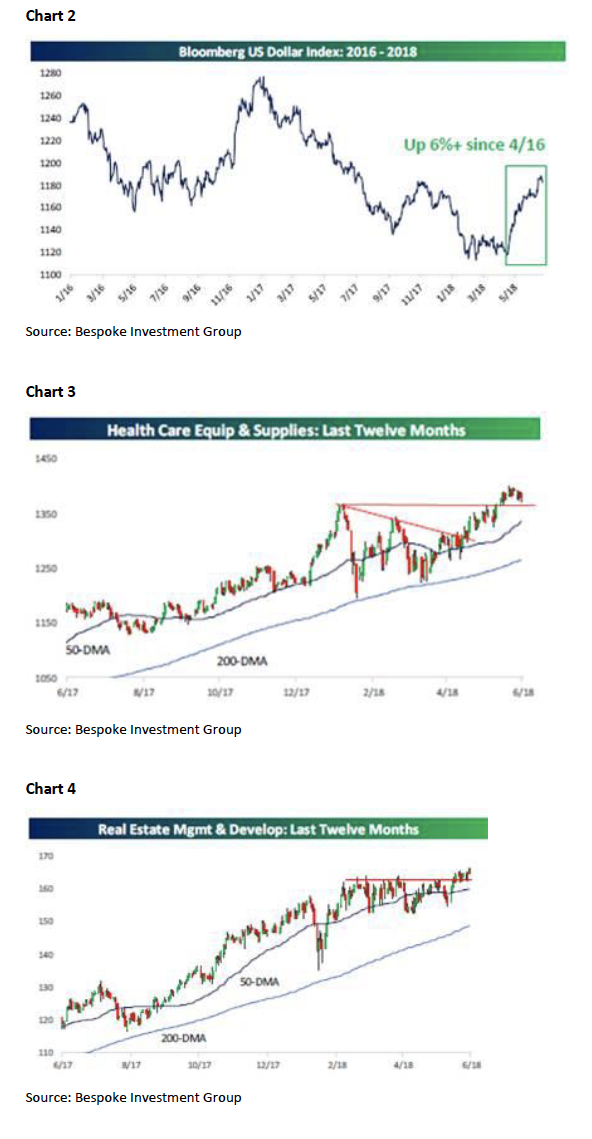

Well, our long-term proprietary model has been positive since October 2008, yet our short/intermediate models are somewhat confused currently, likely spooked by last Tuesday’s wilt. Our short-term momentum indicator is non-trending (read: neutral) and our short-term breadth indicator is also non-trending, even though on an intermediate-term basis the Advance – Decline Line remain very constructive (Chart 1). Admittedly, however, the NASDAQ and Russell 2000 A/D Lines have not “rolled over” like the S&P 500’s A/D has. Another short-term headwind has been the recent economic data where of the 11 economic recent releases, eight of them were missing the estimates. Meanwhile, our April “call” that the U.S. dollar has bottomed remains in force (Chart 2).

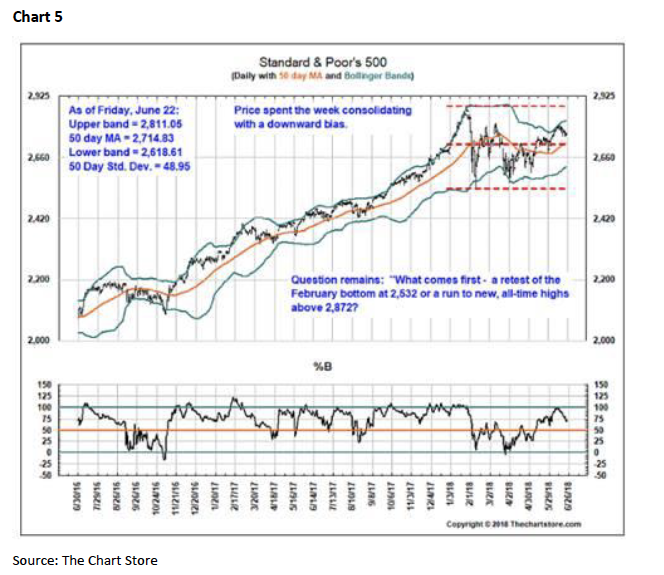

Screening the various industry groups, over the weekend, shows healthcare & equipment has broken out to the upside (Chart

- with Baxter (BAX/$74.32/Outperform) and Merit Medicine (MMSI/$50.40/Outperform) being positively rated by our fundamental analysts and screening well on our proprietary algorithms. Also, real estate management & development (Chart

- has broken out with Jones Lang LaSalle (JLL/$168.83/Outperform) also looking good on our

The call for this week: According to the astute Lowry Research organization:

Since testing its March 9th high, the S&P 500 has continued to pull back modestly. The recent May high, around 2,730, offers the best nearby support on continued weakness with 2,700 as further support. This would be viewed as a buying opportunity in the context of the healthy Supply/Demand and breadth environment.

Plainly, Andrew and I agree and would note that the biggest losing sector on the week was industrials (not good), while the biggest winner was utilities (also, not good). The biggest commodity winner last week was crude oil (+5.52%), and we have been bullish. Believe it or not, the winningest currency was the Mexican Peso (+3.12%). In conclusion, we ask y’all to contemplate Chart 5. Yet this morning (5:11 a.m.) the preopening S&P 500 futures are again off 16 points as European banks and industrial stocks sink on deepening trade disputes, the U.S. limits Chinese investments in U.S. tech companies, and President Trump tweets, “The United States is insisting that all countries that have placed artificial trade barriers and tariffs on goods going into their country, remove those barriers & tariffs or be met with more than reciprocity by the U.S.A. Trade must be fair and no longer a one way street!”