Weekly Market Updates

Random Gleanings at 38,000 Feet

Although Steve is a staunch Republican, he suggested that Republicans worship at the altar of the CBO (Congressional Budget Office). Scoffing, he stated it is ridiculous for ANY government agency to attempt to predict what is going to happen over the next 10 years. Continuing, Steve theorized the Republicans believed that repealing Obamacare would raise enough money to give them more room for tax cuts. However, they lost the public relations battle because the CBO wrongly predicted 22 million people would be thrown off of the health care rolls with such a repeal. He said the CBO starts with the false premise 15 million folks would not pay for healthcare if there was not a mandate and that 5 million would be shoved off of Medicaid. A few more of his random thoughts included: the White House had no clear message in the healthcare debate, there are no real free markets in healthcare, under the current system it does not create an environment to foster medical breakthroughs, and he proposed the following:

- Have flexibility on

- There should be a nationwide shopping system for

- Level the playing field on taxes for

- There should be transparency on pricing by

- Have flexibility on healthcare

To point number four Steve mentioned that in comparing pricing for the same test at various hospitals showed the price varied from $1,400 to $7,300!

Moving on to taxes, he noted the White House, having botched the healthcare debate, will now move on to taxes, but will they really get tax reform? His answer was YES, but first you have to ignore the CBO guidance. Yet the window for big tax reform has passed because too much time was wasted on the healthcare “thing.” What should be done is to cut corporate tax rates, accelerate depreciation, and immediately give taxpayers a “double exemption” (puts an extra $1,400 into their pockets), cut individual tax rates, and make all of that retroactive.

Finally the conversation turned toward “regulations.” Steve averred that unnecessary regulations cost the economy $2 trillion a year and there are 15 bills currently in the House of Representatives to reduce said regulations. Moreover, we should scale back the EPA, FDA, and FAA. In conclusion he opined that regulations would not have prevented the 2008 debacle and the subsequently imposed regulations have prevented the banks from lending somewhere between $1.5 trillion and $2 trillion dollars that typically would have been lent.

We enjoyed spending a few days with Steve Forbes and hope to so again in the not too distant future.

We had another interesting meeting while in Boston with Arvind Navaratnam, portfolio manager of the Fidelity Advisor Event Driven Opportunity Fund (FMRMX/$13.76). We began by asking Arvind why there was a picture of a Boeing B-17 Flying

Fortress in his presentation. He replied, “Because that airplane prompted the first “check list” for an aircraft. I like this story as scribed in Wikipedia:

All of us know the famed B-17 used during WWII, which helped to win the war. You probably didn’t know, however, that the B-17 was the first aircraft to get a checklist! This came about when, on the first B-17 flight, three men were seriously injured, and a few days later died, when the aircraft stalled shortly after takeoff. After further investigation, it was found that the Captain had left the elevator lock on, and the aircraft was unresponsive to pitch control. . . . During a major think-tank

session, it was determined that the pilots needed a checklist. It wasn’t a knock to the pilots, or that the aircraft was too hard to fly, rather the aircraft was just too complex for a one pilot’s memory.

According to Arvind, “In our business a ‘plane crash’ is a permanent loss of capital,” so Arvind uses a “check list” for each stock in his fund to make certain it meets all his requirements. The fund’s model is reflected in the name “event driven.”

Event driven investing attempts to take advantage of corporate actions (index deletions, bankruptcy, corporate spinoffs, 13D filings, mergers, management changes, dividend reductions, etc.) that can result in a mispricing of a company’s stock or other underlying security. These situations can result in forced selling pressure, limited research coverage, and market inefficiencies that can lead to a greater probability of a security being mispriced. As always terms and details should be studied before purchase of the fund.

Moving on to the stock market, despite the S&P 500’s (SPX/2500.23) move to new all-time highs last week, our models

continue to show that there just is not much “upside energy” right here, implying the “buy the North Korea dips” may not work this time. In fact, most of the indices we monitor have moved from neutral, or oversold, into an overbought condition on a short-term basis. That said, one of our overriding themes of the year has been a weaker U.S. dollar. We have been bearish of the “buck” for the last few years, rightly at times and wrongly at others. Still, after a post presidential election rally

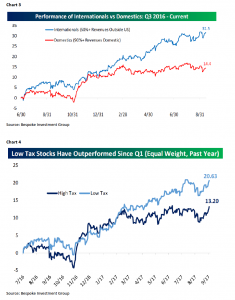

of 6.5% the Bloomberg U.S. Dollar Index has declined by some 10.5% (chart 1 on page 3). The dollar’s weakness has benefited many commodities (chart 2) and we have recommended tilting portfolios accordingly. If the dollar remains “soft” it should continue to benefit companies with international exposure/revenues (chart 3 on page 4). Another theme we have spoken of since DJT was elected is overweighting companies that have a high tax rate on the premise they will benefit from corporate tax reform (chart 4). Some names from the Raymond James research universe with such metrics (they all have an effective tax rate greater than 35%), are favorably rated by our fundamental analysts, and screen well on our models, for your

potential “buy list” include: UnitedHealth (UNH/$198.18/Strong Buy); Dollar General (DG/$77.60/Strong Buy); CSRA (CSRA/$31.98/Outperform); Masco (MAS/$37.31/Outperform); Comcast (CMCSA/$36.93/Strong Buy); and CVS Health (CVS/$83.17/Outperform).

The call for this week: Back in June the three major indices traded out to new all-time highs, and we noted that every time those indices simultaneously trade to new all-time highs the SPX had an average 3.8% gain within the next three months nearly 100% of the time. Well, it is nearly three months later and the SPX is better by some 3.6%. Regrettably, we have underplayed that 3.6% rally because our models went into cautionary mode at the beginning of August. Most recently, our stock market internal energy model telegraphed there just is not a whole lot of upside energy available right here. Then too, the momentum indicator theorizes the odds of a trend reversal are high on a short-term basis, the breadth indicator is neutral (no trend reversal), and the sentiment indicator is flashing extreme complacency (high degree for a trend reversal). The catalyst for a potential near-term trend reversal could be the president’s address at the U.N. this week, where Ambassador

Nikki Haley recently stated, “We’ve been kicking the can down the road, and we’re out of road!” All of this as Kim Jong-un bellows that North Korea is close to its goal of “equilibrium” in military force with the U.S.; and he might just try to demonstrate that coincident with the president’s U.N. address. This morning the preopening S&P 500 futures are up by about 4 points as investors believe the Federal Reserve will announce the trimming of its balance sheet and no North Korea provocations over the weekend.

Important Investor Disclosures

Raymond James & Associates (RJA) is a FINRA member firm and is responsible for the preparation and distribution of research created in the United States. Raymond James & Associates is located at The Raymond James Financial Center, 880 Carillon Parkway, St. Petersburg, FL 33716, (727) 567-1000. Non-U.S. affiliates, which are not FINRA member firms, include the following entities that are responsible for the creation and distribution of research in their respective areas: in Canada, Raymond James Ltd. (RJL), Suite 2100, 925 West Georgia Street, Vancouver, BC V6C 3L2, (604) 659-8200; in Europe, Raymond James Euro Equities SAS (also trading as Raymond James International), 40, rue La Boetie, 75008, Paris, France, +33 1 45 64 0500, and Raymond James Financial International Ltd., Broadwalk, House, 5 Appold Street, London, England EC2A 2AG, +44 203 798 5600.

This document is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The securities discussed in this document may not be eligible for sale in some jurisdictions. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Investors should consider this report as only a single factor in making their investment decision.

For clients in the United States: Any foreign securities discussed in this report are generally not eligible for sale in the U.S. unless they are listed on a U.S. exchange. This report is being provided to you for informational purposes only and does not represent a solicitation for the purchase or sale of a security in any state where such a solicitation would be illegal. Investing in securities of issuers organized outside of the U.S., including ADRs, may entail certain risks. The securities of non-U.S. issuers may not be registered with, nor be subject to the reporting requirements of, the U.S. Securities and Exchange Commission. There may be limited information available on such securities. Investors who have received this report may be prohibited in certain states or other jurisdictions from purchasing the securities mentioned in this report.

Please ask your Financial Advisor for additional details and to determine if a particular security is eligible for purchase in your state.

The information provided is as of the date above and subject to change, and it should not be deemed a recommendation to buy or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. Persons within the Raymond James family of companies may have information that is not available to the contributors of the information contained in this publication. Raymond James, including affiliates and employees, may execute transactions in the securities listed in this publication that may not be consistent with the ratings appearing in this publication.

Raymond James (“RJ”) research reports are disseminated and available to RJ’s retail and institutional clients simultaneously via electronic publication to RJ’s internal proprietary websites (RJ Investor Access & RJ Capital Markets). Not all research reports are directly distributed to clients or third-party aggregators. Certain research reports may only be disseminated on RJ’s internal proprietary websites; however such research reports will not contain estimates or changes to earnings forecasts, target price, valuation, or investment or suitability rating. Individual Research Analysts may also opt to circulate published research to one or more clients electronically. This electronic communication distribution is discretionary and is done only after the research has been publically disseminated via RJ’s internal proprietary websites. The level and types of communications provided by Research Analysts to clients may vary depending on various factors including, but not limited to, the client’s individual preference as to the frequency and manner of receiving communications from Research Analysts. For research reports, models, or other data available on a particular security, please contact your RJ Sales Representative or visit RJ Investor Access or RJ Capital Markets.

Additional information is available on request.