Weekly Market Updates

Smoot-Hawley?

“In March 2002, President George W. Bush imposed a 30% tariff on Chinese steel. The results were chaotic. In a report put out by Consuming Industries Trade Action Coalition in February of that year, the coalition found the tariffs against China boosted the overall prices of steel and cost the U.S. 200,000 jobs in businesses that buy steel, representing $4 billion in lost wages.”

. . . Foundation for Economic Education (3/2/18)

George Wilhelm Friedrich Hegel once stated, “We learn from history that we do not learn from history,” and that quote leaped into our head last Friday. At the time we were speaking to a few hundred investors at a conference. In the Q&A we said the announcement on tariffs on steel and aluminum had been delayed when someone in the audience piped up and said, “The President just imposed them.” Now while this is certainly not like Smoot-Hawley’s tariff on 20,000 imported goods, it is a step in the wrong direction, in our opinion. As The New York Times’ Neal Irwin wrote, “A signal about the willingness of the President to ignore his most sober-minded advisers and put the global economy at risk to achieve his goal of better terms for American trade.” Armed with that thought we dialed up some of our contacts inside the D.C. Beltway and what we heard was discomforting.

The D.C. grapevine has it that the Republicans on The Hill are furious about the tariffs. More importantly, we heard repeatedly that national security advisor Lt. General H.R. McMaster is likely going to leave. Even more shocking is the rumor that Gary Cohn, the Director of the National Economic Council and chief advisor to the President, is probably going to leave after getting overruled on the tariff question. Ladies and gentlemen, if those two leave, can Chief of Staff General Kelly be far behind? Importantly, if they all leave there will be nobody left to say “no” to the President! Again, as Mr. Irwin wrote, “A signal about the willingness of the president to ignore his most sober-minded advisers.”

So what’s the big deal about steel and aluminum? Well, the world’s global steel production is about 1.7 trillion metric tonnes. China is by far the largest producer, accounting for an eye-popping 49% of that 1.7 trillion metric tonnes. As a sidebar, the U.S. produces only 5%. Not surprisingly, the U.S. is the world’s largest importer of steel, at a run rate of 29 billion metric tonnes. However, Canada and Mexico account for much of those steel imports. Ben May, a director at Oxford Economics, said that 88% of Canadian steel exports went to the U.S. in 2016. The same is true for nearly three-quarters of Mexican steel. And there is what we consider to be the real reason for the tariffs. As we stated on CNBC last Friday, “We think the tariffs are a warning shot to Canada and Mexico given the stalled NAFTA talks. And if the President pulls the U.S. out of NAFTA it is not going to be pretty.”

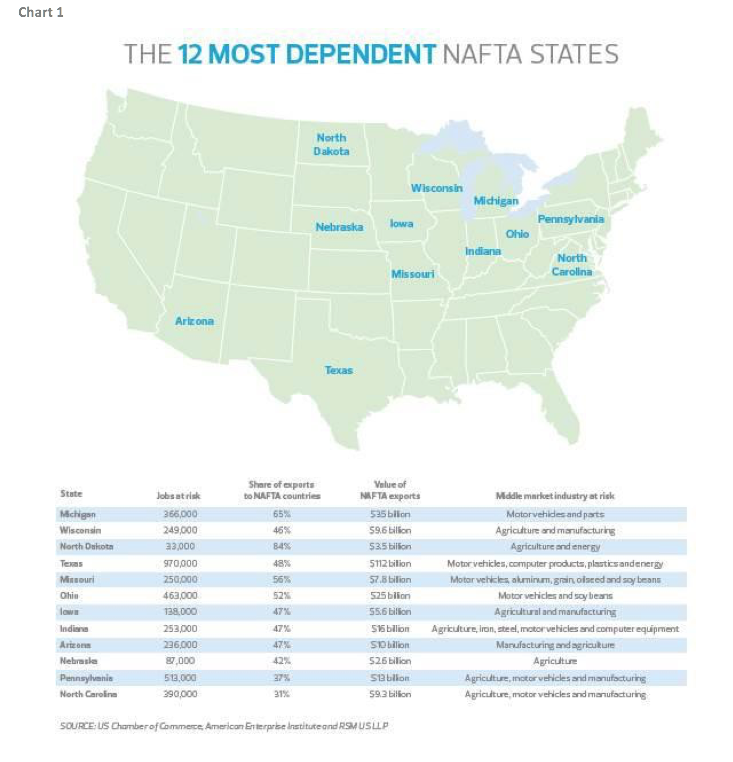

So what’s the deal with NAFTA? Well, according to our pal Joseph Brusuelas, who is the eagle-eyed Chief Economist for RSM, NAFTA is a big deal for the U.S. In a recent presentation Joe notes that there are $312.4 billion worth of U.S. goods exported to Canada from the U.S. and $61.4 billion of U.S. services. Meanwhile, $240 billion worth of U.S. goods are exported to Mexico and $30 billion worth of services. Speaking to the potential jobs impact of pulling out of NAFTA, Joe shows the 12 most affected states (chart 1 on page 3). Take my home state of Michigan. Exiting NAFTA would put 366,000 jobs at risk, mainly in the auto and auto parts sectors. For Texas there are 970,000 potential jobs at risk; so yes, NAFTA is a big deal.

Clearly, the equity markets didn’t like the word “tariff” and responded accordingly with the S&P 500 (SPX/2691.25) sliding from Wednesday’s intraday high of 2761 into Friday’s intraday low of 2696, for a 2.4% decline, before firming into Friday’s closing bell. So where does that leave us in what we thought might just be a “buying stampede,” even though our short-term model suggested last Tuesday’s print high of 2789.15 was the upside “it” on a trading basis. Well, like the stock market has been fickle during the month of February, it depends on which index you want to use. If you use the D-J Industrials, the stampede is over because that index has declined for four consecutive sessions. Using the SPX, however, renders a different verdict, at least as of today, because it has only experienced three consecutive downside sessions. We do find it interesting the SPX bounced on Friday off of its 100-day moving average (DMA) at 2666.56. Yet, we consider the 20-DMA, and 140-DMA, to be more significant moving averages. By studying chart 2 (on page 4) one can see how the 20-DMA has supported the SPX for a long time and what happened when the SPX fell below that moving average in early February. Also note how the 140- DMA ended the “selling squall.” If the tariff-induced selling continues, it will be important to watch the SPX around its 140- DMA currently at 2613, but of course that moving average is now declining. That said, we are still of the belief that the February intraday lows of 2533 will not be retested. As we wrote in Friday’s missive, “Then there was this from Merrill

Lynch’s ex-veteran strategist Bob Farrell, ‘If everyone’s looking for a test of a prior low, either you don’t get a test or, if you do, you shouldn’t buy!’”

The call for this week: As stated in Friday’s Morning Tack, “We didn’t think it would happen, but happen it did as President Trump announced tariffs on steel and aluminum on Thursday.” Subsequently, all day Friday various media outlets asked us what was going to be the impact of said tariffs? We answered by saying, “We don’t know how to analyze the current situation until we learn the extent of other countries’ retaliatory moves.” As we write, the European Union is preparing to impose tariffs on Harley-Davidson motorcycles, bourbon whiskey, and Levi’s jeans in response to the President’s planned tariffs. Canada’s Foreign Minister Chrystia Freeland said that “should restrictions be imposed on Canadian steel and aluminum products, Canada will take responsive measures to defend its trade interest and workers.” While we believe the chances of a significant trade war are low, they still exist; and, if the rest of the world gets tough with the U.S., things could get very rough very quickly. Over the next few weeks the situation should become clearer. Whatever the resolution, we think the pillars of the secular bull market remain in place, which would be earnings and a stronger economy. As our friend Tony Dwyer writes:

Again, we are not getting wrapped up in the reason for the most recent push lower because it isn’t investable until there is clarity on actual policy vs. a statement. We stand ready to become more aggressive buyers as the market retests the low, and especially if it breaks it. We are saying that out loud now, because if it does happen, it will likely be pretty scary. When it is all said and done, the S&P 500 (SPX) correlates with the direction of EPS, and SPX operating EPS are likely to be up 20% this year. We wouldn’t want to get too negative into that kind of EPS bump.

This morning President Trump’s threat of reciprocal tariffs on EU car imports and the Italian election results (hung Parliament) were negatives in Sunday night trading. Instead of the usual buying for Monday as we write, at 5:12 a.m., the preopening S&P 500 futures are off about 2 points.

P.S. – Now that the U.S. is net exporter of energy, a trade war is far less harmful.

Important Investor Disclosures

Raymond James & Associates (RJA) is a FINRA member firm and is responsible for the preparation and distribution of research created in the United States. Raymond James & Associates is located at The Raymond James Financial Center, 880 Carillon Parkway, St. Petersburg, FL 33716, (727) 567-1000. Non-U.S. affiliates, which are not FINRA member firms, include the following entities that are responsible for the creation and distribution of research in their respective areas: in Canada, Raymond James Ltd. (RJL), Suite 2100, 925 West Georgia Street, Vancouver, BC V6C 3L2, (604) 659-8200; in Europe, Raymond James Euro Equities SAS (also trading as Raymond James International), 40, rue La Boetie, 75008, Paris, France, +33 1 45 64 0500, and Raymond James Financial International Ltd., Broadwalk House, 5 Appold Street, London, England EC2A 2AG, +44 203 798 5600.

This document is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The securities discussed in this document may not be eligible for sale in some jurisdictions. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Investors should consider this report as only a single factor in making their investment decision.

For clients in the United States: Any foreign securities discussed in this report are generally not eligible for sale in the U.S. unless they are listed on a U.S. exchange. This report is being provided to you for informational purposes only and does not represent a solicitation for the purchase or sale of a security in any state where such a solicitation would be illegal. Investing in securities of issuers organized outside of the U.S., including ADRs, may entail certain risks. The securities of non-U.S. issuers may not be registered with, nor be subject to the reporting requirements of, the U.S. Securities and Exchange Commission. There may be limited information available on such securities. Investors who have received this report may be prohibited in certain states or other jurisdictions from purchasing the securities mentioned in this report.

Please ask your Financial Advisor for additional details and to determine if a particular security is eligible for purchase in your state.

The information provided is as of the date above and subject to change, and it should not be deemed a recommendation to buy or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. Persons within the Raymond James family of companies may have information that is not available to the contributors of the information contained in this publication. Raymond James, including affiliates and employees, may execute transactions in the securities listed in this publication that may not be consistent with the ratings appearing in this publication.

Raymond James (“RJ”) research reports are disseminated and available to RJ’s retail and institutional clients simultaneously via electronic publication to RJ’s internal proprietary websites (RJ Investor Access & RJ Capital Markets). Not all research reports are directly distributed to clients or third-party aggregators. Certain research reports may only be disseminated on RJ’s internal proprietary websites; however such research reports will not contain estimates or changes to earnings forecasts, target price, valuation, or investment or suitability rating. Individual Research Analysts may also opt to circulate published research to one or more clients electronically. This electronic communication distribution is discretionary and is done only after the research has been publically disseminated via RJ’s internal proprietary websites. The level and types of communications provided by Research Analysts to clients may vary depending on various factors including, but not limited to, the client’s individual preference as to the frequency and manner of receiving communications from Research Analysts. For research reports, models, or other data available on a particular security, please contact your RJ Sales Representative or visit RJ Investor Access or RJ Capital Markets.

Links to third-party websites are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any third-party website or the collection or use of information regarding any website’s users and/or members.

Additional information is available on request.